Research Summary

Adobe’s stock price has collapsed to around $195.16, while the company’s operating performance remains strong. The Million Leaf screenshots show 88.61% gross margin, 36.66% operating margin, 41.45% free cash flow margin, 55.43% ROE, $16.74 basic EPS, and a CAI score of 83, rated Wide. The intrinsic value model estimates $266.31 per share, implying a 26.72% margin of safety.

The market’s concern is clear: generative AI may reduce the need for traditional creative software, weaken Adobe’s pricing power, and shift value from professional workflows to AI-native creation tools. That fear is not irrational. But the latest public evidence does not yet show structural moat impairment. Adobe reported record Q2 FY2026 revenue of $6.62 billion, up 13% year over year, with AI-first ARR more than tripling and exceeding $500 million. It also raised FY2026 revenue and EPS targets.

Million Leaf View: Attractive, but not for reckless all-at-once buying. Adobe is suitable for gradual accumulation because the moat appears intact, the valuation is materially compressed, and the margin of safety is meaningful. The key risk is not current profitability; it is whether AI changes the economic control point of creative workflows over the next 5–10 years.

Layer One: Financial Data — What Happened

The financial screenshots show a company whose market price has weakened far more than its operating economics.

| Metric | Latest Screenshot Data | Interpretation |

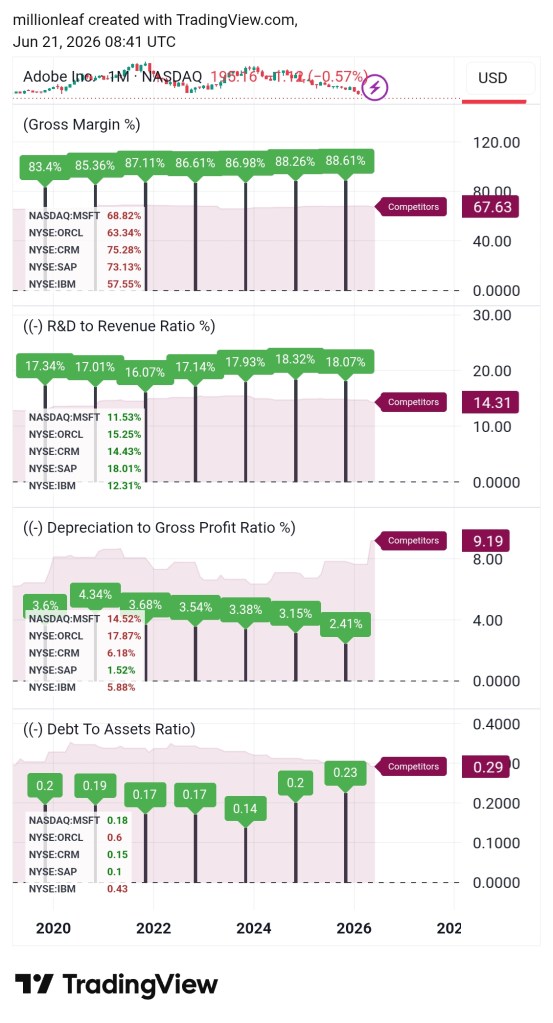

|---|---|---|

| Gross Margin | 88.61% | Extremely high software margin; no evidence of product commoditization yet |

| R&D / Revenue | 18.07% | Elevated but rational; Adobe is reinvesting to defend and extend the platform |

| Depreciation / Gross Profit | 2.41% | Low capital intensity; profits are not dependent on heavy physical assets |

| Debt / Assets | 0.23 | Moderate leverage; not a balance-sheet-driven story |

| Operating Margin | 36.66% | Strong operating quality despite AI investment |

| Free Cash Flow Margin | 41.45% | High cash conversion; earnings are economically real |

| ROE | 55.43% | Strong capital efficiency, partly helped by buybacks and asset-light economics |

| Basic EPS | $16.74 | Earnings power has expanded materially |

The key observation is that Adobe is not showing the normal signs of a business already being disrupted. Gross margin is not collapsing. Operating margin remains above the peer average shown in the screenshot. Free cash flow margin is exceptionally high. EPS has risen from roughly $6.07 in 2020 to $16.74, suggesting that the company has compounded earnings power even while investor sentiment deteriorated.

The weakness is not in current financial production. The weakness is in market trust. Investors are questioning whether today’s margins and cash flows can survive a new AI-native software cycle.

The latest 10-Q supports the screenshot picture. Adobe’s Q2 FY2026 total revenue rose 13% to $6.62 billion, subscription revenue rose 14%, and subscription revenue represented 97% of total revenue. Operating cash flow for the first six months was $5.12 billion, up 10% year over year. This is not a cyclical profit spike or a leverage-driven recovery. It is still a recurring software cash-flow machine.

Layer Two: Business Model — How the Company Makes Money

Adobe makes money by controlling professional and business workflows around content creation, document productivity, digital experience, and marketing execution.

Its core economic engine is subscription software. Customers pay recurring fees for access to Creative Cloud, Acrobat, Adobe Express, Firefly-related AI capabilities, Experience Cloud, Adobe Experience Platform, Adobe Experience Manager, and related enterprise tools. In Q2 FY2026, Creative & Marketing Professionals subscription revenue was $4.54 billion, up 13%, while Business Professionals & Consumers subscription revenue was $1.85 billion, up 16%.

The mechanism is simple but powerful:

Adobe sells tools that become embedded in daily work. Designers, photographers, marketers, agencies, enterprises, students, document-heavy departments, and content teams build habits, files, templates, processes, approvals, and team collaboration around Adobe formats and applications. Once these workflows are embedded, the customer does not merely compare software features. They compare the cost of changing the way work gets done.

That is why gross margin can stay near 89%. Adobe is not selling labor-intensive services. It is selling software, cloud access, workflow control, and creative infrastructure. The marginal cost of serving another subscriber is low, even though AI inferencing and hosting costs are rising. The 10-Q specifically notes that subscription cost of revenue includes hosting, data center, network infrastructure, and AI inferencing costs. The important point is that these costs have not destroyed Adobe’s margin structure.

Adobe earns mainly workflow money and ecosystem-position money. Its cash flow comes from the conversion of recurring subscription revenue into high-margin operating profit, then into free cash flow because the business requires limited capital expenditure relative to revenue.

Layer Three: Underlying Moat — Why the Company Can Make Money Sustainably

The CAI screenshot shows CAI 83, rated Wide. This is consistent with the financial evidence: very high gross margin, strong operating margin, strong free cash flow margin, rising EPS, high ROE, and moderate leverage.

But CAI is evidence, not the conclusion. The real moat comes from several reinforcing sources.

First, Adobe owns professional standards. Photoshop, Illustrator, Premiere Pro, After Effects, InDesign, Acrobat, and PDF-related workflows are not merely products. They are part of how creative and document work is taught, exchanged, reviewed, and delivered.

Second, Adobe benefits from switching costs. A professional designer or enterprise team does not switch only a tool; they switch file compatibility, team knowledge, client expectations, plugin ecosystems, templates, approval flows, archives, and production habits.

Third, Adobe has scale. Its large installed base funds continuous R&D, AI model integration, cloud infrastructure, enterprise sales, and product bundling. The screenshot’s 18.07% R&D-to-revenue ratio is not a sign of distress by itself. In this environment, it is the price of maintaining relevance.

Fourth, Adobe has ecosystem lock-in. Creative Cloud, Acrobat, Express, Firefly, Frame.io, Experience Cloud, and marketing workflows can reinforce one another if Adobe executes well. The Semrush acquisition also signals that Adobe wants to expand its position in marketing intelligence and AI-era brand visibility. Reuters reported that Adobe agreed to acquire Semrush for $1.9 billion to help marketers understand brand visibility across search and generative AI platforms.

The moat stress test is serious. AI can reduce the skill barrier for design. Figma, Canva, OpenAI, Anthropic, Google, Meta, and other AI-native tools can attack parts of the creative workflow. Reuters reported that investors fear autonomous creative tools could hurt demand for traditional software, and specifically noted competitive pressure from Figma and Canva.

However, the threat is more likely to weaken Adobe at the low-end and casual-use layer before it destroys the professional workflow layer. AI can generate images, layouts, drafts, videos, and prototypes. But enterprise-grade creative work still requires brand control, editability, compliance, collaboration, asset management, permissions, legal safety, and integration into production pipelines. Adobe’s opportunity is to make AI a feature inside the workflow rather than letting AI become a substitute for the workflow.

Current moat status: Wide but under active technological stress. The moat is not clearly impaired, but it must be monitored more closely than in the pre-generative-AI era.

Layer Four: Latest News and Dynamic Check — Did Stock Price Movement Damage the Moat?

The recent news has created a sharp gap between business performance and market perception.

Adobe’s Q2 FY2026 results were strong: record revenue, raised full-year guidance, AI-first ARR exceeding $500 million, and Q2 operating cash flow of $2.17 billion. Yet the stock fell because investors are focused on two risks: AI disruption and leadership uncertainty. Reuters reported that the CFO departure came after earlier CEO transition concerns and that shares fell in extended trading despite the guidance raise.

The key recent events are:

| Event | Impact Category | Fundamental Meaning |

|---|---|---|

| Q2 FY2026 beat and guidance raise | Potential moat strengthening | Demand remains healthy; no near-term collapse |

| AI-first ARR tripled to over $500 million | Potential moat strengthening | Early evidence Adobe is monetizing AI |

| CFO departure / leadership transition | Execution risk | Raises uncertainty but does not prove moat damage |

| AI-native creative tools | Competitive pressure | Real long-term threat to pricing and workflow control |

| $25B buyback authorization | Valuation support | Signals confidence in cash flow but does not solve AI risk |

The market is currently worried that Adobe’s historical value capture may be bypassed. If creative output becomes prompt-native and tool-agnostic, Adobe’s seat-based subscription model could face pressure. This is a real risk.

But recent financial evidence does not show that this has already happened. Revenue is growing double digits, subscription revenue remains dominant, RPO remains large, margins are strong, and AI-related ARR is growing quickly. The better classification is:

News Impact: Competitive Pressure + Execution Risk + Potential Moat Strengthening

This is not short-term noise only. AI is a structural test. But it is also not clear moat impairment. The market may be pricing Adobe as if the moat is already broken, while the data still shows a company adapting from a position of strength.

Layer Five: DCF Credibility, Mispricing, and Investment Probability

| Valuation Input | Screenshot Data |

|---|---|

| Current Market Price | $195.16 |

| Million Leaf Intrinsic Value | $266.31 |

| Margin of Safety | 26.72% |

| Free Cash Flow per Share | $23.07 |

| FCF Yield | 11.82% |

| Earnings per Share | $17.48 |

| Earnings Yield | 8.96% |

| Risk-Free Rate | 3.75% |

| Discount Rate | 10.00% |

| Growth Rate | 11.66% |

| Perpetual Growth / P. Growth | 0.12% |

| Dividend Yield | 0.00% |

| Year-1 Cash Flow | $16.49 |

Cash Flow Base Test

The screenshot’s current FCF per share is $23.07, while the DCF year-1 cash flow base is $16.49. That means the DCF does not appear to start from peak current free cash flow. Unless current free cash flow is temporarily inflated, the model’s starting cash flow base is conservative relative to present cash production.

This matters. Adobe’s six-month operating cash flow rose 10% year over year to $5.12 billion, so the cash flow base appears supported by actual operations rather than accounting illusion.

Discount Rate Test

A 10% discount rate is reasonable for Adobe. It is not too generous given AI uncertainty, leadership transition, and competitive pressure. It is also not punitive for a high-margin, recurring-revenue, asset-light software company with moderate leverage. If the discount rate were raised materially, intrinsic value would fall, but the current FCF yield of 11.82% already provides a strong cash-flow anchor.

Growth Rate Test

The model’s 11.66% growth rate is the most sensitive assumption. It is not absurd because Adobe is currently growing revenue around low double digits and raised FY2026 guidance to $26.50–$26.60 billion. But it is not risk-free. For the model to hold, Adobe must continue converting AI into higher ARPU, product expansion, enterprise adoption, and workflow retention.

The growth assumption is credible only if Adobe remains the workflow layer for creative and document production. If AI shifts value away from Adobe’s applications into external AI agents, the growth rate should be reduced.

DCF Credibility Conclusion

The intrinsic value estimate has analytical reference value. The biggest risk is not the cash flow base; it is the durability of growth. The model is not obvious “Garbage In, Garbage Out” because current free cash flow and earnings support the valuation anchor. However, the intrinsic value should be treated as a reasonable base-case estimate, not a certainty.

At $195.16, the stock trades materially below the model’s $266.31 value. The 26.72% margin of safety is meaningful, though not enormous enough to ignore moat risk.

Million Leaf View: Attractive / Fair / Watch / Avoid

Million Leaf View: Attractive

Adobe qualifies as Attractive because the business quality remains high, the CAI indicates a wide competitive advantage, current financial performance remains strong, and the stock price appears to be discounting more structural damage than the evidence currently proves.

However, this should be accumulated gradually, not bought all at once. A reasonable approach is a normal position built in stages, with the first tranche justified at the current price and additional buying tied to evidence that AI adoption strengthens rather than weakens Adobe’s revenue engine.

Position sizing: normal position, not yet core-sized until Adobe proves that AI-first ARR can scale into a larger part of total ARR without margin degradation.

Buying should stop if revenue growth drops below high-single digits while AI-related competition also pressures margins. The position should be reviewed seriously if Creative & Marketing Professionals revenue slows sharply, net retention weakens, or Adobe is forced into aggressive discounting to defend share.

Investment Hypothesis Validation Checklist

Thesis Confirmation Signals

- AI-first ARR continues growing rapidly from the current >$500 million base.

- Creative & Marketing Professionals subscription revenue remains at least high-single-digit to low-double-digit growth.

- Operating margin stays above the mid-30% range despite AI infrastructure costs.

- FCF margin remains around 35–40% or higher.

- Firefly, Express, Acrobat AI Assistant, and Creative Cloud Pro increase ARPU or retention.

- Figma, Canva, and AI-native tools expand the market but do not materially displace Adobe in professional workflows.

- Adobe’s leadership transition stabilizes without strategic drift.

Thesis Break Signals

- Adobe’s gross margin begins falling because AI inference costs cannot be monetized.

- Subscription growth slows sharply despite broader creative AI adoption.

- AI features drive usage but not paid conversion or ARPU.

- Professional creators shift core workflows away from Adobe tools.

- Enterprise customers reduce seats or demand major discounts.

- R&D and sales spending rise while revenue growth decelerates.

- The CAI score declines materially due to weakening margins, FCF conversion, or returns on capital.

Conclusion

Adobe is not a broken company. It is a strong company being priced as if its business model may be bypassed by AI.

That fear deserves respect. AI lowers the barrier to creation, and any company built around creative tools must prove that it still controls the workflow, not merely the old interface. But Adobe’s latest numbers show resilience: high margins, strong cash flow, growing subscription revenue, raised guidance, and early AI monetization.

At the current price, the market appears to be pricing a possible future impairment as though it were already visible in the financial statements. That creates the opportunity. The investment case is not “AI will not hurt Adobe.” The better hypothesis is: AI will pressure Adobe’s old product boundaries, but Adobe’s workflow control, brand standard, installed base, and cash flow allow it to convert AI from a threat into a monetized platform layer.

Final view: Attractive for gradual accumulation, with AI monetization and creative workflow retention as the decisive validation points.

Sources

- Million Leaf internal model screenshots generated on TradingView, dated June 21, 2026.

- Adobe Q2 FY2026 earnings release and SEC exhibit.

- Adobe Q2 FY2026 PDF earnings release.

- Adobe Q2 FY2026 Form 10-Q extract.

- Reuters on Adobe CFO exit, guidance raise, AI ARR, and competitive pressure.

- Reuters on Adobe buyback and AI disruption fears.

- Reuters on FY2026 outlook, Firefly adoption, and Semrush acquisition.