Update Summary

Adobe remains one of the more important companies in the Million Leaf Investment Universe because it combines high financial quality with a clear strategic question: can a deeply embedded creative software incumbent defend its moat in an AI-native content creation environment? The recent market decline has made this question more decision-relevant. At a current market price of $204.02, Adobe is no longer priced as a stable software compounder. The market appears to be discounting a meaningful probability that generative AI weakens the Creative Cloud moat, compresses pricing power, or shifts value toward newer AI-native platforms.

The latest public financial information does not yet show a broken business. Adobe reported record Q2 FY2026 revenue, continued subscription growth, strong operating profitability, and positive AI-related metrics. AI-first ARR exceeded $500 million and tripled year over year, while Adobe raised its FY2026 revenue and non-GAAP EPS targets. That does not eliminate the AI disruption risk, but it does indicate that disruption has not yet translated into visible financial deterioration.

Million Leaf’s internal Competitive Advantage Index assigns Adobe a CAI score of 83, classified as Wide. The score is supported by very high gross margins, strong operating margins, high free cash flow margins, low depreciation burden, manageable interest expense, and strong return on equity. These ratios are consistent with a business that still possesses pricing power, workflow entrenchment, and scalable software economics.

The Million Leaf intrinsic value calculator estimates Adobe’s intrinsic value at $531.05, compared with a current market price of $204.02, implying a margin of safety of 61.58%. The model output suggests that the market price is materially below Million Leaf’s estimate of business value. However, this discount should not be interpreted mechanically. The core issue is not whether Adobe looks statistically cheap. The core issue is whether the market is correctly anticipating moat erosion that is not yet visible in reported financial ratios.

Million Leaf’s current decision tag is Watchlist, Covered, Put Selling Candidate. The thesis remains broadly intact, but it requires active monitoring. Adobe should not be treated as a simple “cheap quality stock” case. It is better understood as a high-quality incumbent facing a structural test: if Firefly, Creative Cloud Pro, Acrobat AI, Express, and enterprise workflow integration reinforce Adobe’s ecosystem, the current valuation may prove overly pessimistic. If AI-native alternatives reduce professional dependence on Adobe’s tools, the apparent margin of safety could be misleading.

What Has Changed

The key change is not that Adobe’s operating performance has collapsed. It has not. The key change is that market confidence has weakened at the same time that Adobe’s reported financials remain strong. That divergence is important. When a high-margin, recurring-revenue software company trades near multi-year lows despite record revenue and raised guidance, the market is usually expressing concern about future durability rather than current results.

The most decision-relevant development is the widening gap between Adobe’s financial quality and investor perception. Public results show continued revenue growth, high cash generation, and expanding AI-related product adoption. Yet the stock price has continued to reflect skepticism around AI monetization, competitive substitution, and management transition. CFO Dan Durn’s departure after the Q2 FY2026 earnings announcement adds another monitoring point, although it does not by itself change the business thesis.

Adobe’s strategic response to AI is also becoming clearer. The company is not positioning Firefly as a separate AI tool outside the Adobe ecosystem. It is embedding AI across Photoshop, Illustrator, Premiere, Acrobat, Express, GenStudio, and enterprise customer experience workflows. This matters because Adobe’s moat is not only the quality of any single model. Its moat depends on whether AI increases productivity inside existing workflows where Adobe already controls customer behavior, file formats, collaboration habits, brand assets, and enterprise content systems.

The central question for this update is therefore not whether generative AI is a risk. It clearly is. The question is whether AI is currently weakening Adobe’s moat in observable financial data. Based on the latest financial ratios and public operating results, the answer is not yet. The risk remains forward-looking, but the financial engine is still functioning.

Financial Quality Review

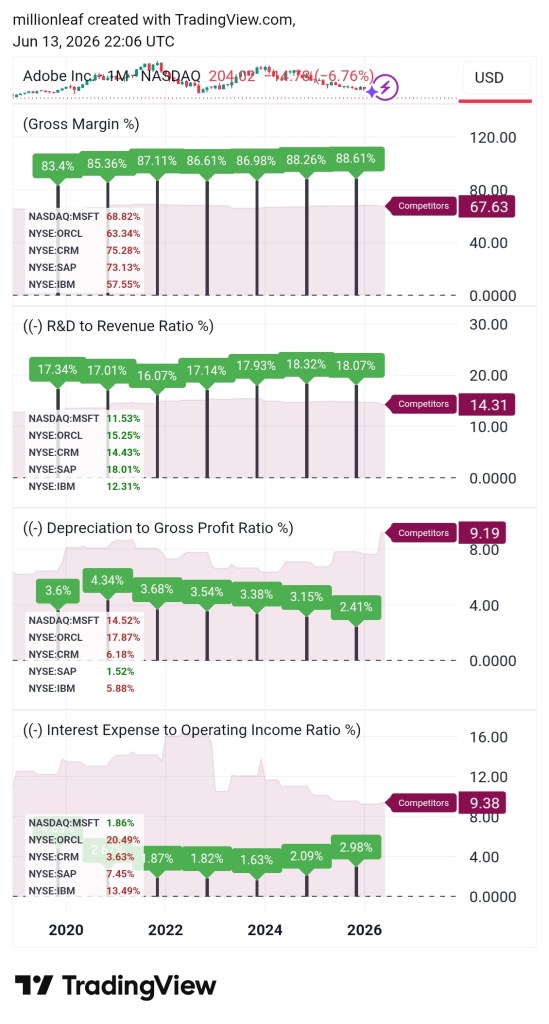

Adobe’s financial ratios continue to support the view that this is a high-quality software business rather than a weakening or commodity-like business. The company’s gross margin remains exceptionally high at 88.61%, above the peer benchmark of 67.63% used in Million Leaf’s model. This is one of the clearest signals of software economics. A company with this level of gross margin is not merely selling a replaceable product at thin spread. It is converting intellectual property, software infrastructure, brand strength, and workflow dependence into highly profitable revenue.

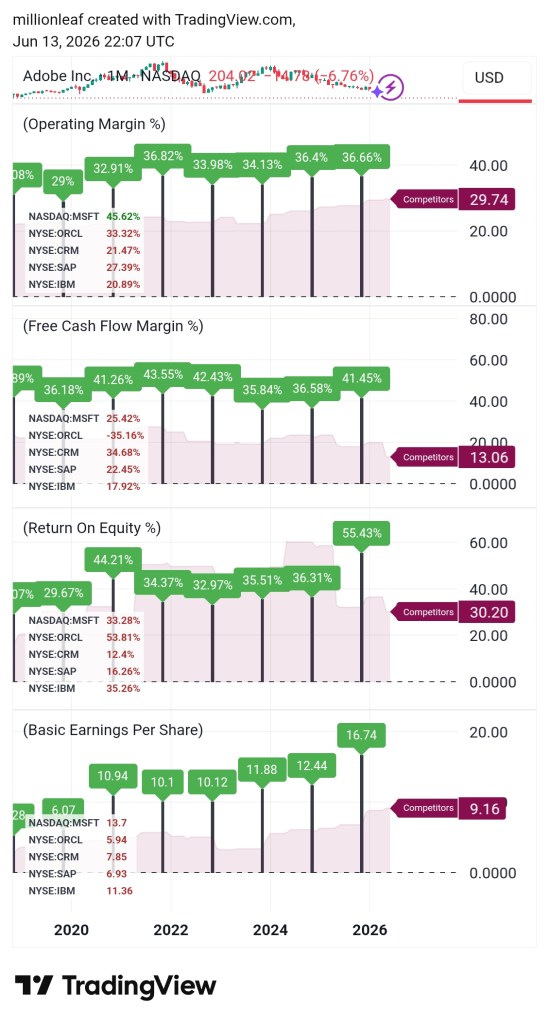

Operating margin is also strong at 36.66%, compared with a peer benchmark of 29.74%. This matters because Adobe is investing aggressively in AI, product development, enterprise go-to-market, and customer acquisition, yet still produces high operating profitability. A high operating margin alongside elevated R&D spending suggests that Adobe has enough economic surplus to defend and extend its platform while still generating attractive profit.

Free cash flow margin is especially important for Million Leaf’s framework. Adobe’s free cash flow margin stands at 41.45%, far above the peer benchmark of 13.06%. This indicates that the accounting earnings are supported by real cash generation. It also gives Adobe flexibility to reinvest, acquire capabilities, repurchase shares, and absorb competitive pressure without immediately weakening its balance sheet or operating structure.

Return on equity is elevated at 55.43%, while basic EPS has increased to 16.74 in the internal model data. These figures reflect a business with strong profitability and capital efficiency. Return on equity should not be interpreted in isolation because buybacks and balance sheet structure can influence the denominator. Still, combined with strong free cash flow, high margins, and low capital intensity, the ratio supports the broader conclusion that Adobe remains an economically strong franchise.

Several cost structure indicators are also favorable. Depreciation to gross profit is only 2.41%, well below the peer benchmark of 9.19%, which confirms that Adobe is not a capital-heavy business. Interest expense to operating income is 2.9%, significantly below the peer benchmark of 9.38%, indicating that the company’s operating income is not materially burdened by financing costs. R&D to revenue is 18.07%, above the peer benchmark of 14.31%, which should be viewed carefully. Higher R&D intensity reduces short-term reported profitability, but for Adobe it is strategically necessary. In an AI transition, underinvestment would be more concerning than disciplined reinvestment.

Overall, the ratios support the view that Adobe remains a high-quality, cash-generative, low-capital-intensity software business. The data does not currently indicate financial deterioration. The more important risk is whether future competition changes the economics before it appears in margins, retention, or free cash flow.

Competitive Advantage Index Review

Million Leaf’s Competitive Advantage Index assigns Adobe a score of 83, placing it in the Wide category. This is an important signal because the CAI is not based on narrative alone. It reflects the financial behavior of the business over time. A wide CAI score suggests that Adobe’s competitive advantage is visible in the numbers: high margins, strong returns, low capital intensity, durable cash conversion, and limited financing burden.

The strongest contributors to the CAI appear to be gross margin, operating margin, free cash flow margin, return on equity, low depreciation burden, and low interest burden. These are the marks of a scalable software franchise. Adobe is not earning high returns because of a short-term accounting benefit or a temporary product cycle alone. It has a business structure that allows revenue to scale across a large subscriber base while incremental software delivery costs remain relatively low.

The CAI also confirms the business narrative. Adobe’s products are embedded in professional and enterprise workflows. Creative professionals, marketers, agencies, enterprises, students, and business users often build habits, files, templates, training, and collaboration processes around Adobe tools. Those switching costs are reflected in Adobe’s ability to maintain premium margins.

The weaker point is not currently in the historical ratios. The weaker point is forward-looking. CAI is designed to capture observed financial advantage, but AI disruption may first appear in user behavior before it appears in margins. Early signs would include slower Creative Cloud net new ARR, higher churn among individual creators, weaker pricing acceptance, lower conversion from free to paid products, or pressure from AI-native design and video tools. For now, the CAI supports the conclusion that the moat remains intact, but it does not remove the need for monitoring.

Business Mechanism and Moat Interpretation

Adobe makes money because its software sits inside the production system of digital work. A designer does not simply buy Photoshop as a standalone application. A team builds workflows around Adobe files, Adobe libraries, Adobe fonts, Adobe collaboration systems, PDF exports, client expectations, and professional standards. A marketing department does not simply buy Adobe Experience Cloud as a dashboard. It integrates customer data, campaign workflows, creative production, analytics, personalization, and content supply chains into Adobe’s enterprise software environment.

This workflow depth is the source of Adobe’s pricing power. The cost of Adobe software is often small relative to the value of professional output. For a designer, agency, publisher, media team, or enterprise marketer, the bigger cost is not the subscription fee. It is the cost of lost productivity, retraining, file incompatibility, workflow disruption, and quality risk. That is why Adobe has historically been able to convert creative software leadership into recurring subscription revenue.

The AI risk challenges this mechanism. If generative image and video tools allow users to bypass professional workflows entirely, Adobe’s moat weakens. If a marketer can generate finished assets in a browser-based AI system without needing Photoshop, Illustrator, or Premiere, the value of Adobe’s traditional toolset could be reduced. If younger creators build habits around simpler AI-native platforms, Adobe’s training and habit moat could erode over time.

However, disruption is not only about technology capability. It is also about workflow adoption. Adobe’s advantage is that Firefly is being placed inside the tools customers already use. This gives Adobe a path to convert AI from a substitute into a feature layer. If AI makes Photoshop faster, Premiere more productive, Acrobat more useful, Express more accessible, and GenStudio more valuable for enterprise content production, AI may reinforce Adobe’s ecosystem rather than destroy it.

Enterprise customers also care about brand safety, rights management, compliance, data governance, integration, and auditability. This is where Adobe may have an advantage over pure AI-native tools. A consumer may experiment with any AI image generator. A global enterprise needs controlled content workflows, permissioning, commercial-use confidence, brand consistency, and integration with marketing systems. Adobe’s moat is therefore stronger in professional and enterprise environments than in casual consumer creation.

The most important interpretation is that Adobe’s moat is evolving. Historically, it was built on professional tools, file standards, brand, training, and workflow dominance. Going forward, it must also be built on AI integration, enterprise trust, content supply chain control, and the ability to monetize productivity gains without alienating users. The moat is not broken, but it is being tested.

Valuation and Margin of Safety

Million Leaf’s intrinsic value calculator estimates Adobe’s intrinsic value at $531.05. Against the current market price of $204.02, this implies a margin of safety of 61.58%. The model also shows a free cash flow yield of 11.31% and an earnings yield of 8.57%, compared with a risk-free rate assumption of 3.75%. Under Million Leaf’s framework, this is a significant valuation gap.

The valuation does not appear to require heroic assumptions if Adobe’s current cash flow quality remains intact. A business with high gross margins, strong operating margins, recurring revenue, low capital intensity, and durable free cash flow can justify a higher intrinsic value than the current market price if the moat remains structurally sound. The current price implies that the market is either applying a severe disruption discount or assuming that future growth and pricing power will be materially lower than the historical financial profile suggests.

That is why the margin of safety should be interpreted as conditional rather than automatic. If Adobe’s moat remains durable and AI becomes an enhancement layer inside Adobe’s ecosystem, the current discount appears substantial. If AI reduces the need for Adobe’s professional tools, compresses subscription pricing, or shifts content creation workflows away from Adobe, then the intrinsic value estimate may need to be revised downward in future updates.

Within Million Leaf’s system, the current valuation supports high-priority monitoring and possible structured entry consideration, but not blind conviction. The Watchlist and Put Selling Candidate tags are appropriate because the market price is far below the internal value estimate, while the business still shows strong financial quality. However, position sizing discipline remains essential. A wide margin of safety is valuable only if the underlying business assumptions remain valid.

Investment Decision Framework

From a business quality perspective, Adobe remains strong. The company has recurring subscription revenue, high margins, strong free cash flow, low capital intensity, and significant reinvestment capacity. These are characteristics Million Leaf generally favors.

From a competitive advantage perspective, Adobe still shows evidence of a durable moat. The CAI score of 83 supports a Wide rating, and the financial ratios confirm that the business has not yet lost pricing power or profitability. The moat is based on ecosystem control, professional workflow dependence, enterprise integration, brand strength, product breadth, and customer habit formation.

From a valuation perspective, the current market price offers a large implied margin of safety relative to Million Leaf’s intrinsic value estimate. However, the discount exists for a reason. The market is questioning whether Adobe’s historical advantage can survive AI-native competition. This is exactly the type of situation where Million Leaf’s Investment Stratagem framework is useful. The goal is not to predict the next price movement. The goal is to determine whether the structure of the opportunity is favorable enough to justify capital exposure under uncertainty.

The favorable structure is clear: strong business quality, wide CAI, large free cash flow yield, and a major discount to estimated intrinsic value. The uncertainty is also clear: AI may change the economics of content creation faster than Adobe can monetize it. Therefore, the correct posture is disciplined, not emotional. Adobe deserves continued coverage and higher watchlist priority, but exposure should be sized around thesis risk.

The key decision trigger is evidence that AI is either reinforcing or weakening the core subscription engine. If AI-first ARR continues to grow, Creative Cloud retention remains healthy, Digital Media ARR expands, and margins stay resilient, the investment thesis strengthens. If revenue growth slows despite AI adoption, pricing power weakens, churn rises, or users migrate to AI-native tools outside Adobe’s ecosystem, the thesis weakens.

Investment Hypotheses to Monitor

Hypothesis 1: Adobe can convert AI disruption into ecosystem reinforcement rather than moat erosion.

What would confirm it: AI-first ARR continues to grow, Firefly adoption expands inside Creative Cloud and Express, and Adobe maintains strong subscription growth.

What would weaken it: AI adoption rises but paid subscription growth slows, suggesting that AI usage is not converting into durable monetization.

Hypothesis 2: Creative Cloud remains difficult to replace for professional users.

What would confirm it: Stable or improving Creative & Marketing Professionals subscription revenue, strong renewal behavior, and continued adoption of premium Creative Cloud plans.

What would weaken it: Accelerating migration to lower-cost or AI-native design and video platforms, especially among agencies, freelancers, and younger creators.

Hypothesis 3: Adobe can defend high free cash flow margins while investing heavily in AI.

What would confirm it: Free cash flow margin remains structurally high, operating margin stays resilient, and R&D investment does not create persistent margin compression.

What would weaken it: AI infrastructure costs, sales costs, or competitive pricing pressure materially reduce cash conversion.

Hypothesis 4: Enterprise workflow integration creates a stronger moat than consumer AI tools alone.

What would confirm it: Growth in GenStudio, Experience Platform, Acrobat AI, and enterprise customer experience workflows.

What would weaken it: Enterprises adopt competing AI content platforms that bypass Adobe’s workflow layer.

Hypothesis 5: The intrinsic value gap remains valid under conservative assumptions.

What would confirm it: Revenue growth, margins, and free cash flow remain consistent with Million Leaf’s valuation framework.

What would weaken it: A structural decline in growth, lower pricing power, or a downward revision in normalized cash flow assumptions.

Key Risks

The first major risk is AI substitution. If AI image, design, and video generation tools become good enough to replace large portions of Adobe’s traditional workflow, Creative Cloud pricing power could weaken. This risk is most relevant among non-professional creators, small businesses, and price-sensitive users.

The second risk is monetization uncertainty. Adobe may successfully drive AI usage but fail to convert that usage into durable paid revenue. High AI engagement without subscription expansion would suggest that AI is increasing product activity without improving economics.

The third risk is margin pressure. AI features may require higher infrastructure spending, model development costs, and go-to-market investment. If Adobe must spend heavily to defend its position while facing pricing pressure, the current high-margin profile could deteriorate.

The fourth risk is competitive bypass. Competitors do not need to replicate the full Adobe suite to pressure the business. They only need to capture specific workflows, such as social media design, AI-generated marketing images, short-form video creation, document automation, or enterprise content generation.

The fifth risk is management and execution. CFO transition increases the need to monitor capital allocation, margin guidance, and communication discipline. Adobe’s business model remains strong, but strategic execution is critical during an AI platform shift.

The sixth risk is valuation model error. A large margin of safety can create false comfort if the underlying assumptions are outdated. If AI permanently lowers Adobe’s growth rate or terminal pricing power, intrinsic value would need to be revised.

Million Leaf Intelligence Conclusion

This update suggests that Adobe’s investment thesis remains intact but contested. The financial evidence continues to support a high-quality, wide-moat software franchise. The CAI score of 83, strong margins, high free cash flow generation, low capital intensity, and large implied margin of safety all support continued inclusion in the Million Leaf Investment Universe.

At the same time, Adobe should not be treated as a risk-free compounder. The market’s skepticism is focused on a real strategic question: whether generative AI strengthens Adobe’s workflow ecosystem or weakens the need for its traditional tools. Current financial results do not show moat collapse, but the risk is forward-looking and must be monitored through subscription growth, AI monetization, retention, margin resilience, and competitive displacement.

The appropriate Million Leaf status remains Watchlist, Covered, Put Selling Candidate. The current valuation appears attractive under Million Leaf’s intrinsic value framework, but any capital deployment should remain disciplined and conditional on evidence that Adobe’s AI strategy is reinforcing rather than eroding the economic engine.

This Intelligence Update reflects Million Leaf’s current assessment based on available business, financial, competitive, and valuation information. The company will continue to be monitored through future updates as new decision-relevant evidence becomes available.